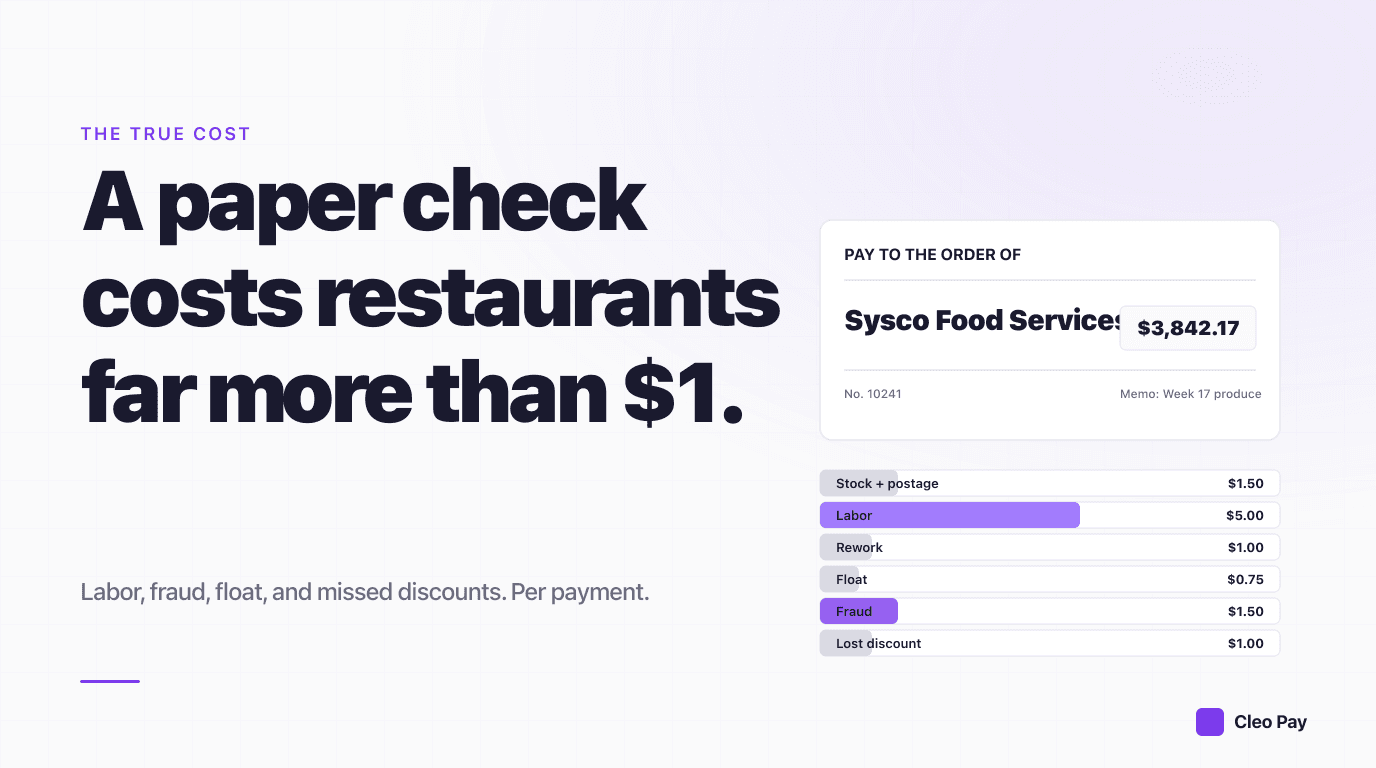

Walk into most restaurant back offices on a Friday and you will see the same scene: a stack of paper checks next to a sheet of stamps, a pen, and a GM signing her way through vendor payments to Sysco, the linen company, and the uniform service. It has been the default for decades and most operators assume it is the cheap option. The stock is 10 cents. The stamp is 73 cents. What could be cheaper?

Almost anything, once you add up the hidden costs. The 2024 AFP Payments Cost Benchmarking Survey puts the fully-loaded cost of a single check at $4 to $20 depending on the business, and that is before fraud exposure. Restaurants tend to cluster at the high end because of the labor model and vendor volume.

Use the calculator below to get your own number, then we will walk through each cost layer.

The direct costs (the ones you can see)

Let us start with what you actually buy when you pay a vendor by check.

Direct cost: roughly $1.00 - $2.00 per check.

This is the number most operators have in their head. If you stop here, checks look like the cheapest rail available. The problem is this number ignores where the actual cost sits.

The hidden costs (the ones that kill you)

1. Labor

Cutting, signing, stuffing, stamping, and mailing a check takes time. Industry benchmarks put it at 7-12 minutes of staff time per check once you include:

- Pulling the bill for payment

- Printing the check

- Getting the signature (often requires walking to the owner or waiting for them to be on-site)

- Stuffing and sealing the envelope

- Stamping and mailing

- Logging it in the system

- Reconciling it when it clears

At a blended hourly cost of $28-$45 (fully loaded, including taxes and benefits for whoever is doing this, typically a bookkeeper or office manager), that is $3.25 to $9.00 in labor per check.

2. Errors and rework

Checks get lost in the mail. Vendors call asking where their payment is. Checks get stolen out of mailboxes. Checks get stale-dated and need to be reissued. A realistic error rate is 2-5% of checks requiring some form of rework, and each rework event adds 15-30 minutes of labor plus potentially a stop-payment fee ($25-$40 at most banks).

Amortized across all checks: $0.50 to $2.00 per check in rework cost.

3. Float mismanagement

Checks settle unpredictably. Some vendors cash immediately, some sit on checks for weeks. That means your cash forecast is fuzzy. For most small restaurants this is invisible. For groups with tight working capital, unexpected check clearance on a slow week can trigger overdraft fees or force expensive short-term borrowing.

Hard to quantify per-check, but easily $0.50-$1.50 per check when averaged across the year.

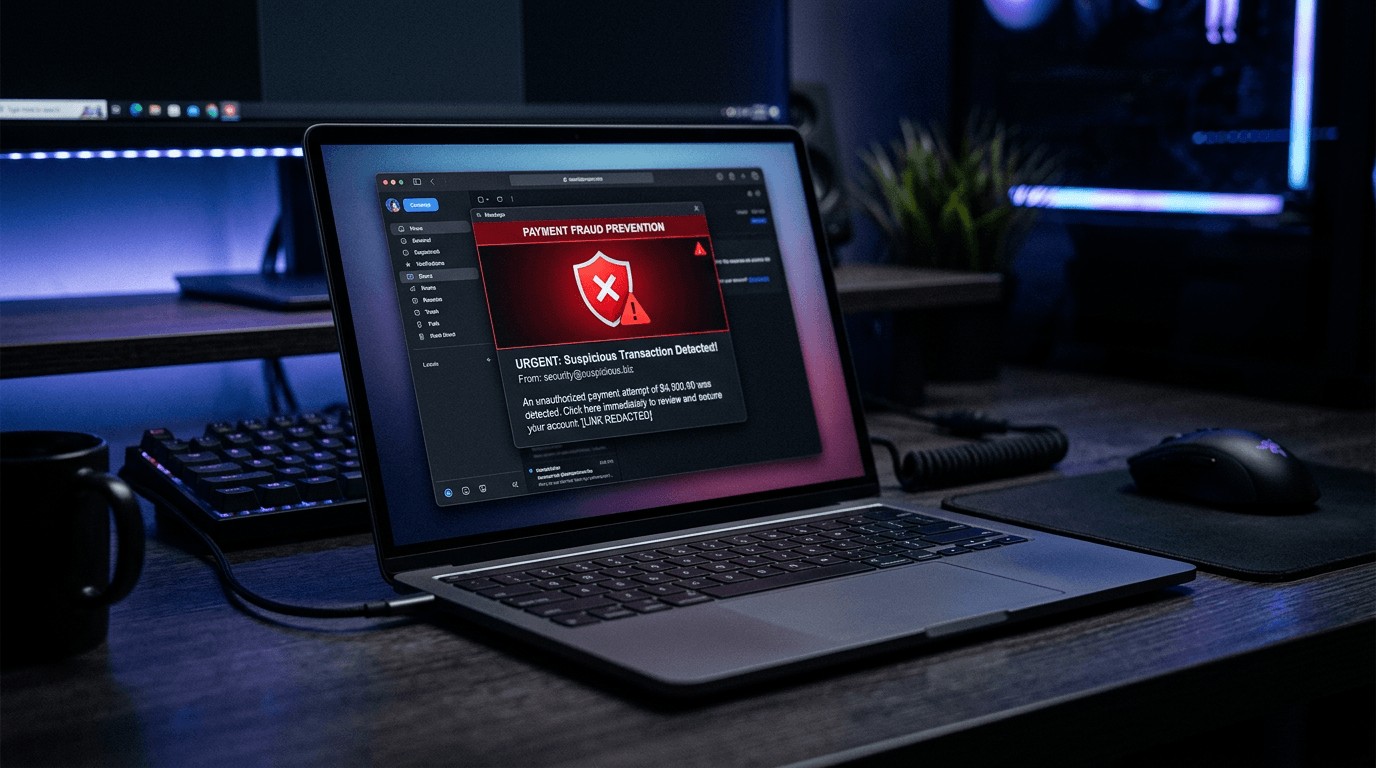

4. Fraud exposure

This is the big one. Checks remain the single most-targeted payment method for fraud. The 2025 AFP Payments Fraud and Control Survey reports that the majority of organizations experienced check fraud attempts in the prior year, with a meaningful percentage of those attempts succeeding.

Restaurant-specific fraud patterns we see:

- Mail theft. Checks stolen from the restaurant's outbound mail or the vendor's inbound mail, then washed and altered. A $450 check to a produce vendor becomes a $45,000 check to "Cash."

- Vendor impersonation. Fraudster intercepts a check destined for Southern Glazer's or Sysco, opens a fraudulent deposit account in that vendor's name, cashes the check.

- Insider fraud. Blank check stock accessible to the wrong staff member.

See our payment fraud prevention guide for a deeper treatment.

5. Missed early-pay discounts

Many vendors offer 2% net 10 terms (pay within 10 days, get 2% off). Checks are too slow and unpredictable to reliably capture these discounts. ACH captures them easily. On a restaurant spending $80,000/month with vendors, that can be $1,600/month or roughly $0.50-$1.50 per invoice in missed savings (depending on mix).

The total: $6 to $22 per check

Adding it up for a typical independent restaurant:

The range across operators is wide. A tight, single-unit operator with a trusted bookkeeper and low fraud exposure might land at $6. A multi-location group with higher labor costs and bigger fraud exposure can easily land above $20.

The comparable fully-loaded cost for an ACH payment, even at retail pricing from a bill pay platform, is typically $0.50 to $1.50. Checks cost 5-15x what ACH costs, once you count everything.

Rail comparison at a glance

- Speed

- 3–10 days + cash float

- Cost

- $6–$22 fully loaded

- Best for

- Holdout vendors who refuse ACH. Should be the exception.

- Speed

- 1–3 business days

- Cost

- $0.50–$1.50

- Best for

- Default rail for 70–85% of restaurant vendor payments.

- Speed

- Instant

- Cost

- Can be net positive (0.75–1.5% rebate)

- Best for

- Vendors who accept cards. Turn AP into a revenue source.

When a check is still the right answer

Not every payment should move to ACH on day one. Checks remain the right call for:

- Vendors who refuse ACH. Some landlords, some very small local suppliers, some cash-basis service providers.

- One-off emergency payments to a new vendor you have not onboarded yet.

- Rebate or refund checks going back to customers.

- Payments to individuals without bank account info yet.

- State-specific liquor three-tier constraints. In some states, certain payment structures to distributors require specific instruments or payment terms. Southern Glazer's and RNDC can advise on what their state requires.

The goal is not to eliminate checks. The goal is to make them the exception, not the default. Most restaurants we talk to can get from 60-80% checks to 10-20% checks inside 90 days.

A concrete example: a 3-location group

Consider a three-unit restaurant group paying 180 invoices a month across all three locations. Today, 70% go out by check (126 checks/month) and 30% by ACH.

Today's cost:

- 126 checks × $10.75 = $1,354.50/month

- 54 ACH payments × $1 = $54/month

- Total AP payment cost: $1,408.50/month or $16,902/year.

After moving to 15% checks / 85% ACH:

- 27 checks × $10.75 = $290.25/month

- 153 ACH × $1 = $153/month

- Total: $443.25/month or $5,319/year.

Annual savings: ~$11,583. That is before counting fraud exposure reduction, which is not a line item until the day it becomes one.

Use the calculator at the top of this post to plug in your own numbers.

The transition plan

Moving off checks is a project, not a flip. A sequence that works:

- Sort your vendors by payment volume. The top 20% will account for 80% of your check spend. Focus there first. Sysco, PFG, Baldor, Southern Glazer's, linen, R&M vendors are common top entries.

- Collect banking info. Email each top-20% vendor and ask for their ACH info. Most will respond within a week. Use a bill pay tool that verifies bank ownership via micro-deposit or Plaid, do not just trust the email.

- Hold checks for laggards. For vendors who refuse or drag their feet, keep checks for now. Revisit quarterly.

- Move one vendor at a time. Do not try to flip everyone at once. The first ACH cycle for each vendor, double-check that the payment landed before you celebrate.

- Add virtual card where accepted. Some national vendors (Toast subscription, EcoLab chemicals, software) accept virtual card and you earn rebates on the spend. Net cost can be negative.

- Reserve checks for the short tail. Within 90 days, checks should be a small minority of your payment mix.

How Cleo Pay helps the transition

Cleo Pay is built to make this move low-friction:

- Vendor portal for ACH collection with bank ownership verification.

- All rails in one workflow, so moving a vendor from check to ACH is a settings change, not a tool change.

- Printed-and-mailed checks for the short tail of vendors who still require them, without you having to touch a stamp.

- Fraud controls (positive pay, dual control, vendor bank change alerts) active by default.

- Discount capture on early-pay terms.

See Cleo Pay for restaurants to see how this works end to end.

FAQ

The bottom line

Checks are not free. They are one of the most expensive payment rails your restaurant uses, once you count labor, errors, float, fraud, and missed discounts. The $10.75/check number is conservative, and it adds up to real money even for single-unit operators.

The move off checks is not about being modern. It is about stopping the quiet bleed and removing one of the biggest fraud vectors from your business. If you are still paying most of your vendors by paper, 2026 is the year to change that.