If you run a restaurant group, hotel, or event production company, you probably work with dozens of independent contractors every year. Freelance photographers, DJ crews, contract maintenance workers, pop-up chefs, event staff agencies. Every one of them may trigger a 1099 filing requirement, and missing even one can mean IRS penalties that eat into your margins.

This guide breaks down exactly what hospitality businesses need to know about 1099 compliance in 2026: which forms to file, who qualifies as a contractor, critical deadlines, and how to build a system that handles it all without burying your back office in paperwork.

Understanding 1099-NEC vs. 1099-MISC

The IRS uses two primary 1099 forms that apply to hospitality businesses, and confusing them is one of the most common mistakes we see.

1099-NEC (Nonemployee Compensation)

Use the 1099-NEC for any non-employee you paid $600 or more during the tax year for services. In hospitality, this covers:

- Freelance chefs and culinary consultants brought in for menu development, pop-up dinners, or seasonal menus

- DJs, musicians, and entertainers booked for events

- Freelance photographers and videographers hired for marketing shoots or event coverage

- Independent maintenance and repair contractors who handle plumbing, HVAC, or equipment servicing

- Event production freelancers like lighting designers, sound engineers, and stage managers

- Consulting services including food safety auditors, interior designers, and marketing consultants

The key test: did you pay a non-employee $600+ for services rendered? If yes, file a 1099-NEC.

1099-MISC (Miscellaneous)

The 1099-MISC covers a narrower set of payments in hospitality:

- Rent payments of $600 or more to a landlord who is not a corporation (think: a restaurant leasing space from an individual property owner)

- Royalty payments exceeding $10

- Prizes and awards worth $600+ (relevant for hospitality businesses that run contests or competitions)

- Gross proceeds to attorneys of $600 or more

A common scenario: your restaurant group leases a second location from a private landlord. That rent payment gets reported on a 1099-MISC, Box 1. Meanwhile, the freelance chef you brought in for a private dining series gets a 1099-NEC.

Who Counts as a Contractor in Hospitality?

Misclassifying workers is one of the most expensive compliance mistakes a hospitality business can make. The IRS uses a multi-factor test that evaluates three categories.

Behavioral Control

Does your business control how the worker does their job? If you dictate specific procedures, provide detailed training, or require the worker to follow your step-by-step methods, they're likely an employee. If you define the end result but the worker decides how to get there, that points toward contractor status.

Example: A hotel hires a freelance interior designer to refresh the lobby. The hotel says "we want a modern, coastal aesthetic" but lets the designer choose materials, source furniture, and manage the timeline. That's a contractor. But if the hotel assigns the designer specific tasks daily, requires them to work on-site during set hours, and supervises every decision, the IRS may view them as an employee.

Financial Control

Does the worker have a significant investment in their own equipment? Can they realize a profit or loss? Do they offer services to other businesses? Contractors typically provide their own tools, carry their own insurance, and serve multiple clients.

Example: A DJ who owns their sound system, carries liability insurance, has their own LLC, and performs at multiple venues is clearly a contractor. A "house DJ" who uses the venue's equipment, works every Friday and Saturday on a fixed schedule, and has no other clients looks more like an employee.

Relationship Type

Is there a written contract? Does the worker receive benefits? Is the relationship ongoing or project-based? Permanent, benefits-eligible arrangements suggest employment. Defined-scope, project-based engagements suggest contractor status.

Common Hospitality Contractor Roles

Here's a quick reference for roles that are typically classified as independent contractors in hospitality:

When in doubt, consult a tax professional. The penalties for misclassification can include back taxes, interest, and penalties going back multiple years.

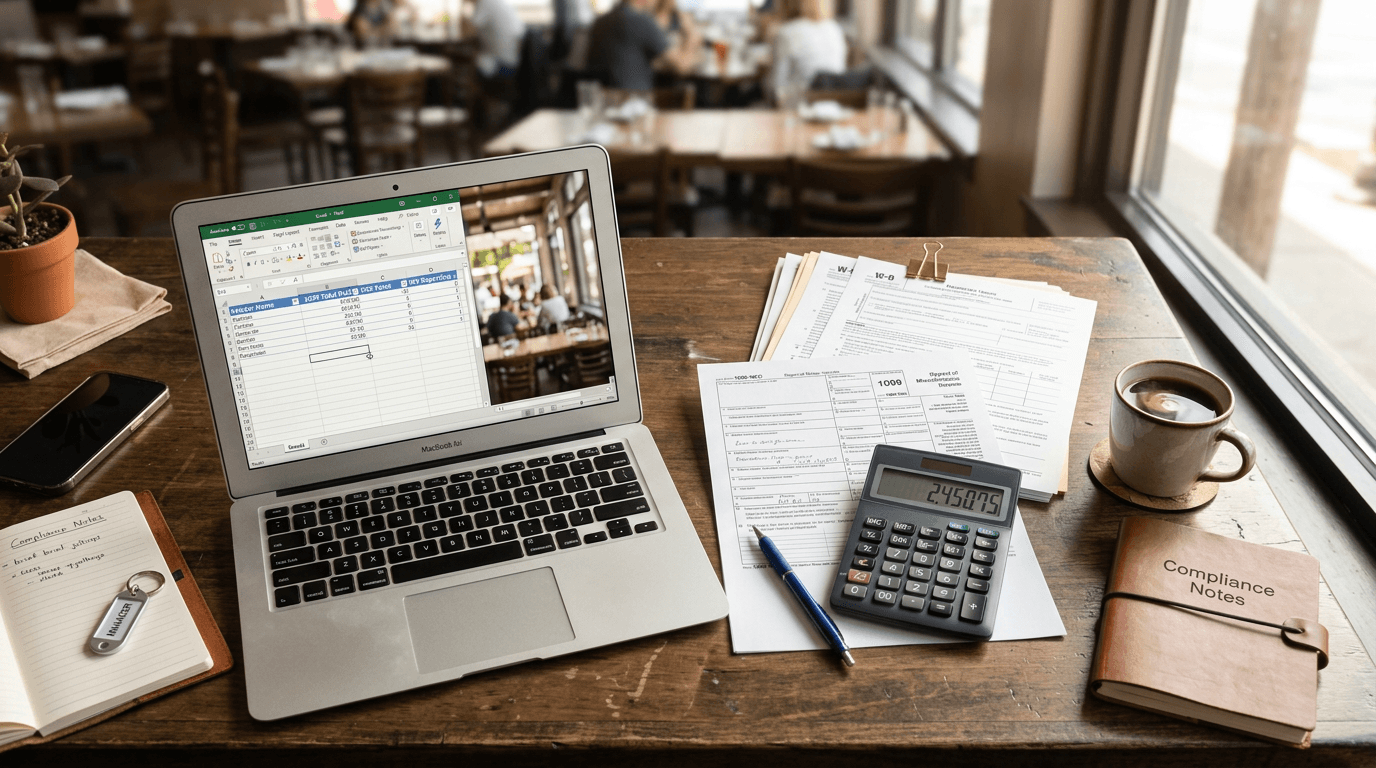

Filing Deadlines and Key Dates for 2026

Missing a 1099 deadline is not a gray area. The IRS applies penalties per form, per day late, and they add up fast across dozens of contractors.

Critical Dates

- January 31, 2027: Deadline to furnish 1099-NEC copies to recipients AND file with the IRS. This is the same date for both, with no automatic extension available for 1099-NEC forms.

- February 28, 2027: Deadline to file 1099-MISC with the IRS if filing on paper.

- March 31, 2027: Deadline to file 1099-MISC with the IRS if filing electronically.

- January 31, 2027: Deadline to furnish 1099-MISC copies to recipients.

The Calendar You Should Actually Follow

Smart hospitality operators don't wait until January to think about 1099s. Here's the timeline that prevents last-minute scrambles:

October-November 2026: Audit your vendor list. Identify every contractor paid $600+ year-to-date. Flag any missing W-9s.

December 2026: Send W-9 requests to any contractors with missing or outdated forms. Verify TINs through IRS TIN matching. Reconcile payment records across all locations.

January 1-15, 2027: Generate 1099 forms. Review for accuracy. Resolve any TIN mismatches.

January 16-31, 2027: Distribute copies to contractors. File with the IRS electronically.

Penalties for Non-Compliance

The IRS penalty structure scales based on how late you file and the size of your business. For 2026 tax year filings:

- Filed within 30 days of deadline: $60 per form

- Filed after 30 days but by August 1: $130 per form

- Filed after August 1 or not at all: $330 per form

- Intentional disregard: $660 per form with no maximum cap

For a mid-size restaurant group working with 40 contractors, failing to file on time could mean $13,200 in penalties at the $330 tier. That's money straight off your bottom line for a paperwork failure.

Small Business Exception

Businesses with gross receipts of $5 million or less have reduced maximum penalties. But "reduced" still means up to $660,000 per year for late filing and $1,319,500 for intentional disregard. These are not trivial numbers.

Building a 1099 Compliance System

Manual 1099 management breaks down as soon as a hospitality business crosses about 15-20 contractors per year. Here's what a reliable compliance system looks like.

Step 1: Centralize Your Vendor Data

Every contractor relationship should start with a complete record: legal name, business entity type, TIN, address, and W-9 on file. If you're managing vendors across multiple locations, this data needs to live in one place.

Step 2: Collect W-9s Before the First Payment

The single best compliance habit is collecting a W-9 before you cut the first check. Once you've paid a contractor without their W-9, you're chasing paperwork with zero leverage. For a detailed breakdown of this process, see our step-by-step W-9 collection guide.

Step 3: Validate TINs Proactively

The IRS TIN Matching Program lets you verify that a contractor's name and TIN match IRS records before you file. A mismatch on a submitted 1099 triggers a B-Notice process that creates months of administrative headaches.

Step 4: Track Payments Against the $600 Threshold

Your system needs to aggregate payments per contractor across all locations and payment methods. A contractor who receives three $250 payments across two of your locations has crossed the $600 threshold, and that's easy to miss without centralized tracking.

Step 5: Automate Form Generation and Filing

Manually preparing 1099s in January is how errors happen. Automated systems pull from your payment records, populate forms, validate data, and file electronically.

Ready to simplify your AP workflow?

Get early access to Cleo Pay and see how we help hospitality teams save hours every week.

How Cleo Pay Handles 1099 Compliance

We built Cleo Pay specifically for hospitality businesses that manage dozens of contractor relationships across locations. Here's how the platform handles the compliance workflow end-to-end.

Automated W-9 Collection

When you add a new vendor to Cleo Pay, the platform automatically sends a secure W-9 request. Contractors fill out the form digitally, and their information is validated and stored. No PDFs floating around in email threads, no chasing paper forms before year-end.

Real-Time Payment Tracking

Every payment processed through Cleo Pay is tagged to the vendor and location. The platform continuously tracks cumulative payments against the $600 threshold and flags contractors who are approaching or have crossed it. You can see your 1099 liability at any point during the year, not just in January.

TIN Verification

Cleo Pay validates contractor TINs when they're submitted, catching mismatches months before you need to file. This eliminates the B-Notice cycle that wastes hours of administrative time.

One-Click 1099 Generation

When filing season arrives, Cleo Pay generates your 1099-NEC and 1099-MISC forms from your payment data. Review, approve, and file electronically, all from one dashboard. The platform also distributes contractor copies automatically.

Multi-Location Consolidation

For restaurant groups and hotel management companies operating across multiple entities, Cleo Pay consolidates contractor payments across locations. A vendor who works at three of your properties gets one accurate 1099 reflecting all payments, not three incomplete ones.

Common 1099 Mistakes in Hospitality

After working with hundreds of hospitality businesses, we see the same errors repeatedly.

Paying Corporations and Still Filing 1099s

Payments to C-corporations and S-corporations generally do not require 1099 reporting (with exceptions for legal and medical services). If your linen service provider is an incorporated business, you don't need to file a 1099. The W-9 tells you the entity type.

Ignoring Credit Card Payments

Payments made via credit card or third-party payment networks (like PayPal or Stripe) are reported by the payment processor on Form 1099-K. You do not also report these on a 1099-NEC. Only payments made by check, ACH, cash, or wire transfer trigger your 1099-NEC obligation.

Using Old W-9s

W-9 forms don't technically expire, but contractor information changes. A contractor who incorporated their business last year needs to submit an updated W-9 reflecting their new entity type and EIN. Best practice is to request updated W-9s annually.

Forgetting About One-Time Vendors

That photographer you hired once in March for $800? They need a 1099-NEC. One-time engagements above $600 are easy to forget when you're compiling year-end records, especially if the payment was processed outside your normal AP workflow.

Getting Started

1099 compliance doesn't have to be a January fire drill. With the right systems in place, you can handle contractor payments and reporting as a natural part of your operations.

Start by auditing your current contractor relationships. Identify anyone missing a W-9. Centralize your payment records. And if you're ready to automate the entire workflow, see how Cleo Pay works for hospitality businesses managing contractors across locations.

The cost of non-compliance is real and measurable. The cost of getting it right, with the right tools, is a fraction of a single penalty notice.